PREIT Reports Second Quarter 2020 Results

Operations suspended for an average of 86 days

Results reflect closure for majority of quarter

All malls reopened as of July 3, 2020

PREIT (NYSE: PEI) today reported results for the three and six months ended June 30, 2020. A description of each non-GAAP financial measure and the related reconciliation to the comparable GAAP financial measure is located in the tables accompanying this release.

“We continue to be appreciative of our PREIT associates for executing on all aspects of our plan to get through this challenging period. Our resolve in creating the best overall consumer experience remains,” said Joseph F. Coradino, Chairman and CEO of PREIT. “Long before this pandemic hit, we were responding to changes in consumer behavior. Our properties have superior market positioning as dominant retail hubs and we believe they will continue to gain market share as we strengthen them into commerce districts that include apartments, hotels, storage and last-mile fulfillment, medical and other uses. Our go-forward capital allocation priorities are to ensure that only the best opportunities to bolster our underlying earnings stream are pursued.”

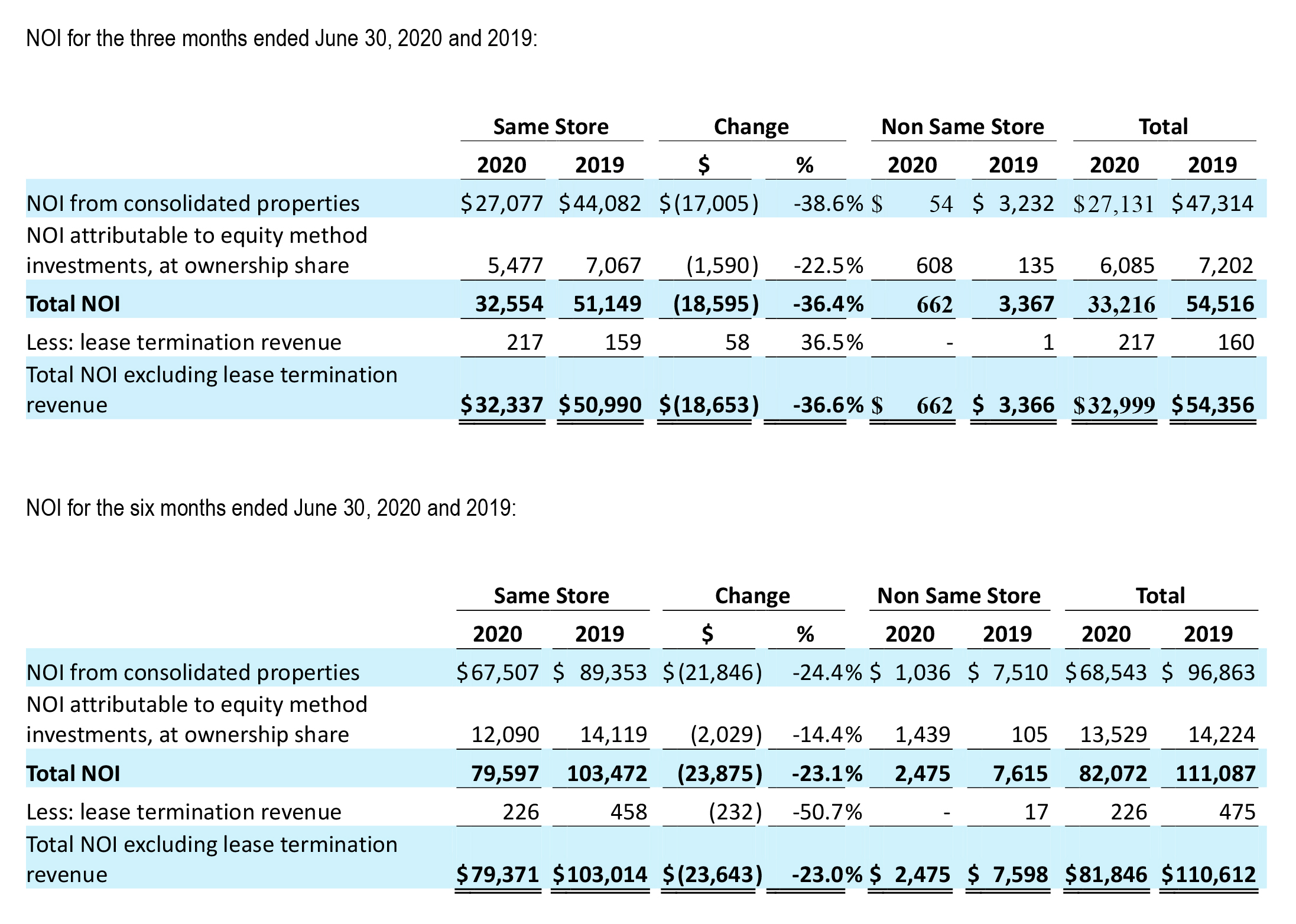

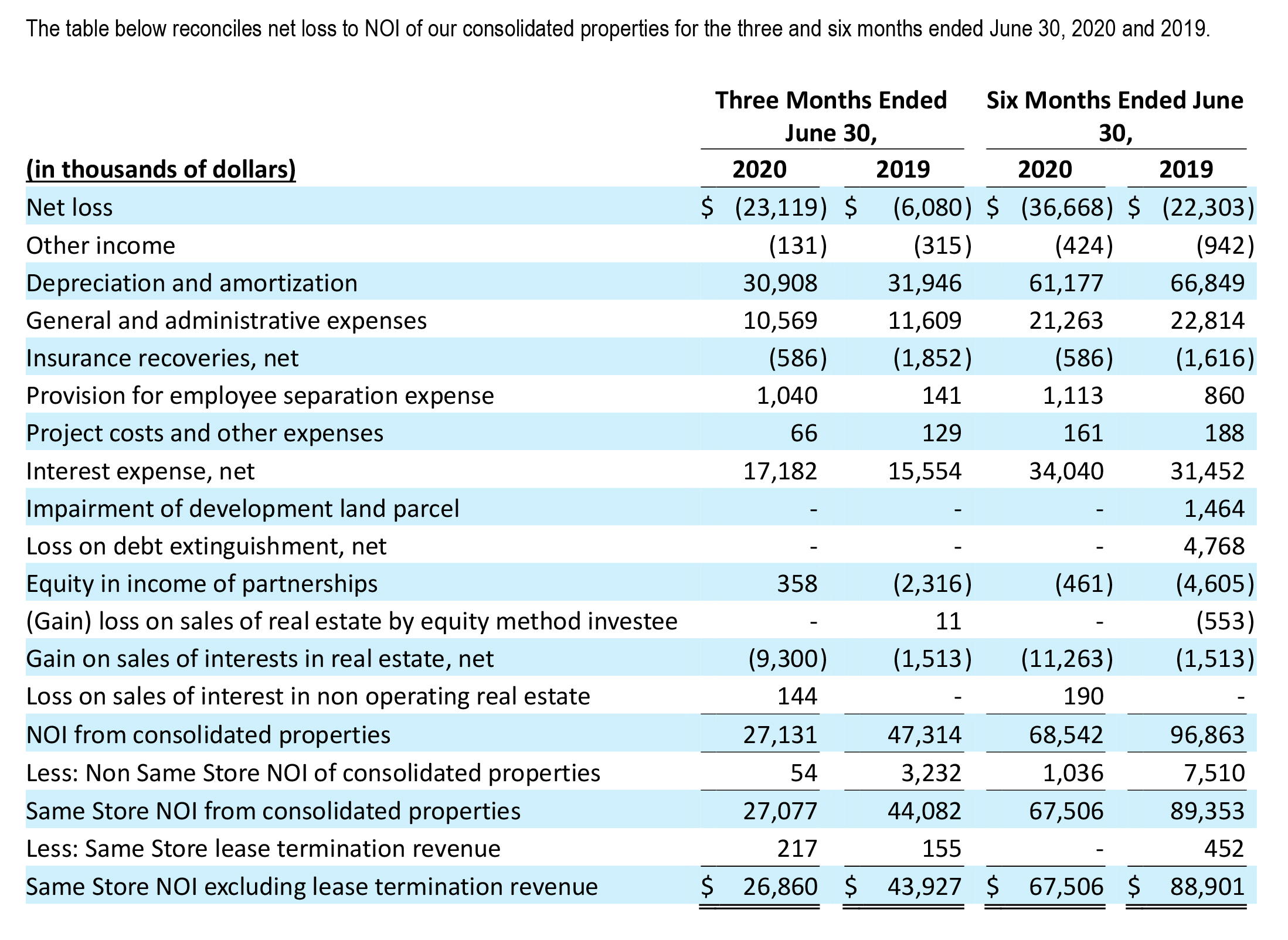

Same Store NOI, excluding lease termination revenue, decreased 36.6% for the three months ended June 30, 2020 compared to June 30, 2019.

The quarter was impacted by a decrease in revenue of $20.1 million primarily resulting from bankruptcies and related store closings, an increase in credit losses for challenged tenants, the accounting for rental abatements as well as decreased percentage sales revenue resulting from mall closures related to the COVID-19 pandemic.

Core Mall total occupancy was 92.4%, a decrease of 130 basis points compared to June 30, 2019. Core Mall non-anchor occupancy declined by only 40 basis points from last year despite the impact from bankruptcies and chain liquidations that resulted in 12 store closures for an aggregate 59,000 square feet during the first six months of 2020.

Non-anchor Leased space, at 90.3%, exceeds occupied space by 80 basis points when factoring in executed new leases slated for future occupancy, excluding Fashion District Philadelphia.

Average renewal spreads for the quarter in our wholly-owned portfolio were 2.3% for spaces less than 10,000 square feet.

The Company continues to make progress on liquidity-generating capital transactions including its multifamily and hotel land sales and the multi-property sale-leaseback transaction. During June, the Company completed the remaining outparcel sales, generating $14.4 million.

On July 27, 2020, the Company executed amendments to its Senior Credit Facilities that, among other things, suspended certain financial covenants effective as of June 30, 2020 until August 31, 2020, subject to extension until September 30, 2020 if the Company meets certain conditions. The Company continues its discussions with lenders to agree upon a longer-term financing solution before August 31, 2020.

Leasing and Redevelopment

Excluding Fashion District Philadelphia, 197,000 square feet of leases are signed for 2020 openings, which is expected to contribute annual gross rent of $11.7 million.

Key openings at recent redevelopment completions continue including: Kate Spade, Industrious and Francesca’s at Fashion District Philadelphia; Talbot’s Outlet, Restore Cryotherapy and Plymouth Performing Arts Center at Plymouth Meeting Mall; and Sephora and Jamba at Woodland Mall.

Property Re-openings and COVID-19 Response

As of July 3, 2020, all of PREIT’s malls have re-opened, excluding certain prohibited uses that vary by state.

Core mall physical in-line occupancy registered 83.1% as of August 7, 2020.

Core mall traffic at comparable properties is approximately 68% of 2019 non-holiday averages.

Cash collections for April through July totaled 53% of billings.

Deferral agreements have been reached with 60% of PREITs key national tenants by number.

As part of the Company’s plan to improve liquidity during the COVID-19 crisis, the Company has executed on corporate actions: In addition to previous one-time savings in G&A and operating expenses totaling $4.7 million, PREIT made permanent overhead reductions, that are expected to save the Company approximately $4.0 million annually in G&A expenses. Planned 2020 capital spending was reduced by $26 million. We also received deferral on approximately $11.6 million in real estate tax payments and entered into agreements that provide for forbearance or loan modifications on mortgage loans for eight of our properties.

In continuous support of its tenants, PREIT has developed and implemented its own contactless pick up solution, Mall2Go, and has developed a branded parking lot activation series, Park and Play, that will result in nearly two dozen events being held between late July and mid-September across its portfolio.

Across its portfolio, the Company has hosted blood drives and food donation drives, provided meals to area essential workers, and donated much needed protective supplies. Read more about our efforts here.

Shop Local webpages were developed by PREIT, aggregating ecommerce sites for all the small businesses throughout our portfolio. The offerings highlighted these businesses not only to the local audience, but to customers of the entire PREIT portfolio, leveraging the Company’s marketing power for local business partners.

Through PREIT’s SBA resources page and contact with tenants, the Company has continued to provide resources for smaller businesses to access the liquidity needed to make it through this challenging time.

PREIT’s mall websites now include job portals to collect information to pass along to our retail partners.

Primary Factors Affecting Financial Results for the Three Months Ended June 30, 2020 and 2019:

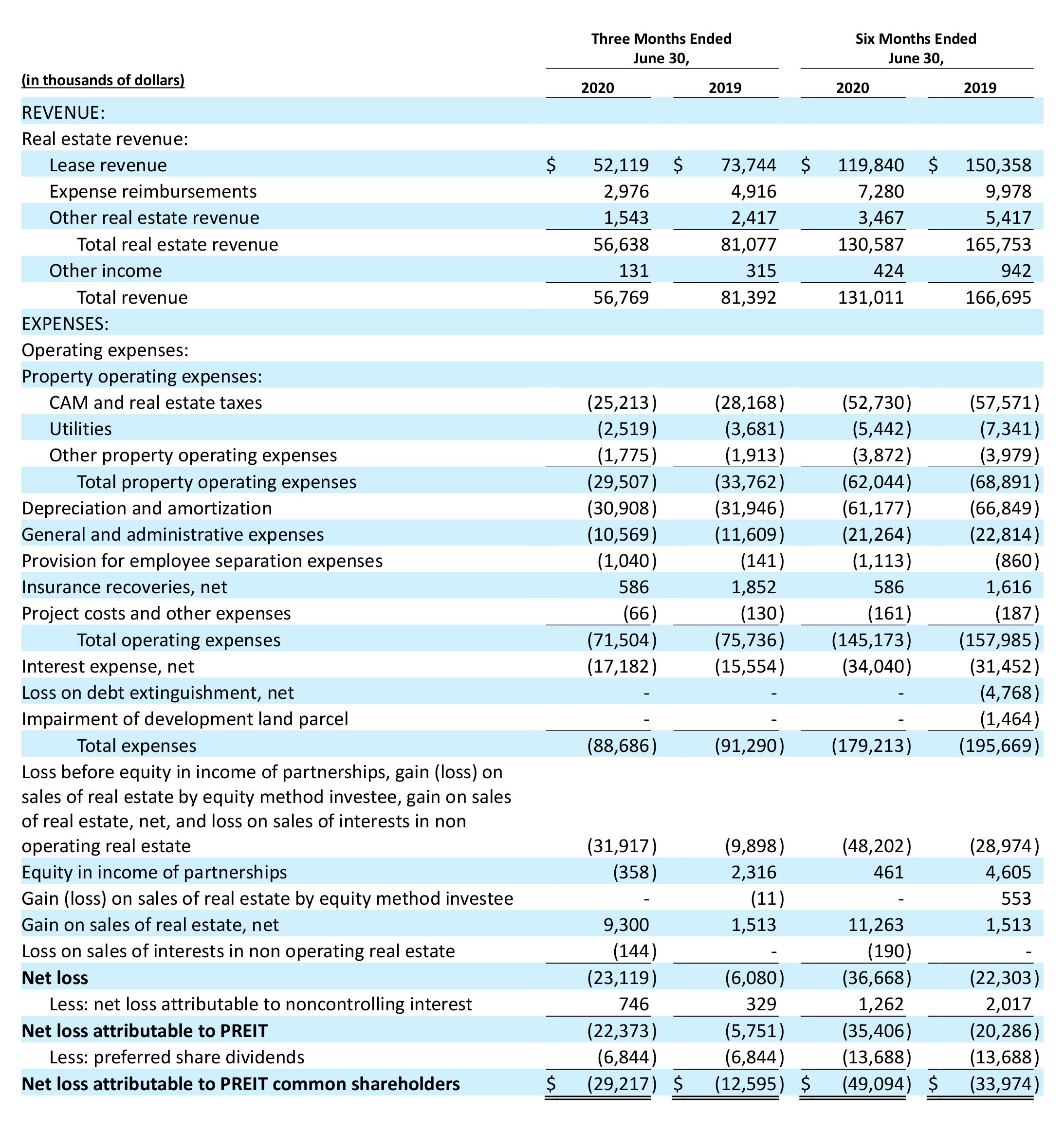

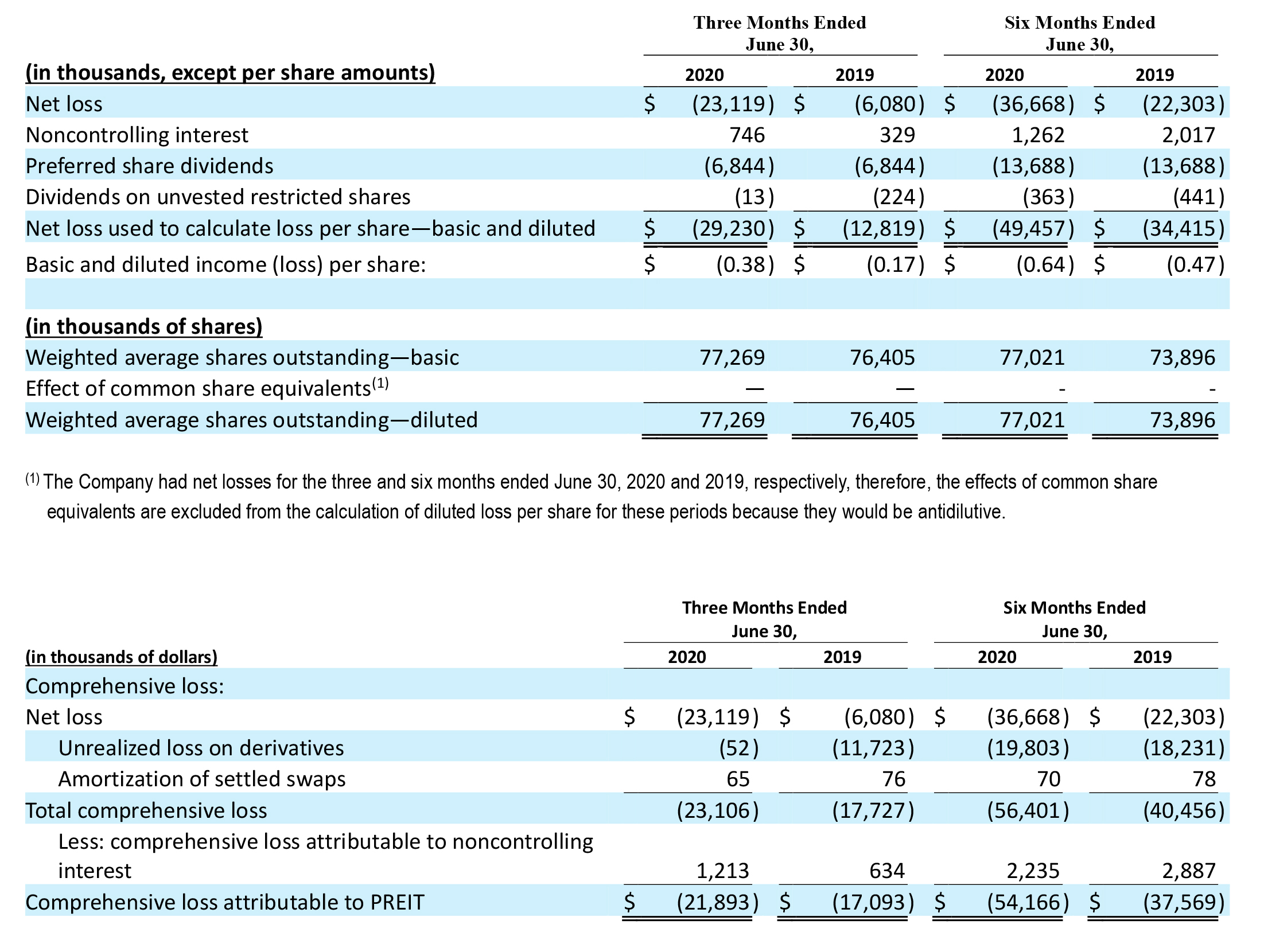

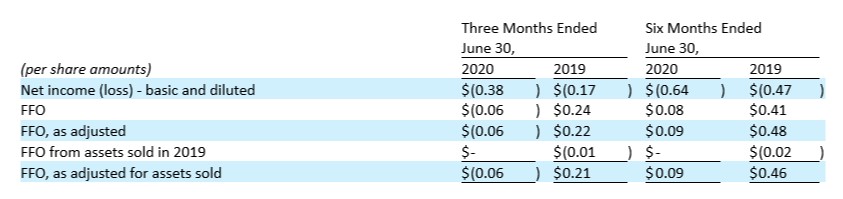

Net loss attributable to PREIT common shareholders was $29.2 million, or $0.38 per basic and diluted share for the three months ended June 30, 2020, compared to net loss attributable to PREIT common shareholders of $12.6 million, or $0.17 per basic and diluted share for the three months ended June 30, 2019.

Same Store NOI decreased by $18.6 million, or 36.4%. The decrease is primarily due to lost revenues from bankrupt tenants, an increase in credit losses, accounting for rental abatements and a decrease in percentage of sales revenue due to COVID-19 related mall closures, partially offset by new store openings, including contributions from replacement anchors.

Non Same Store NOI decreased by $2.7 million, primarily due to lost revenues from bankrupt tenants, an increase in credit losses and a decrease in percentage of sales revenue due to COVID-19 related mall closures. Other decreases in NOI from Non Same Store properties is due to the conveyance of Wyoming Valley Mall and lower contributions from Exton Square Mall, resulting from an anchor closing and related co-tenancy revenue adjustments, as well as the sale of an outparcel during the second quarter of 2019.

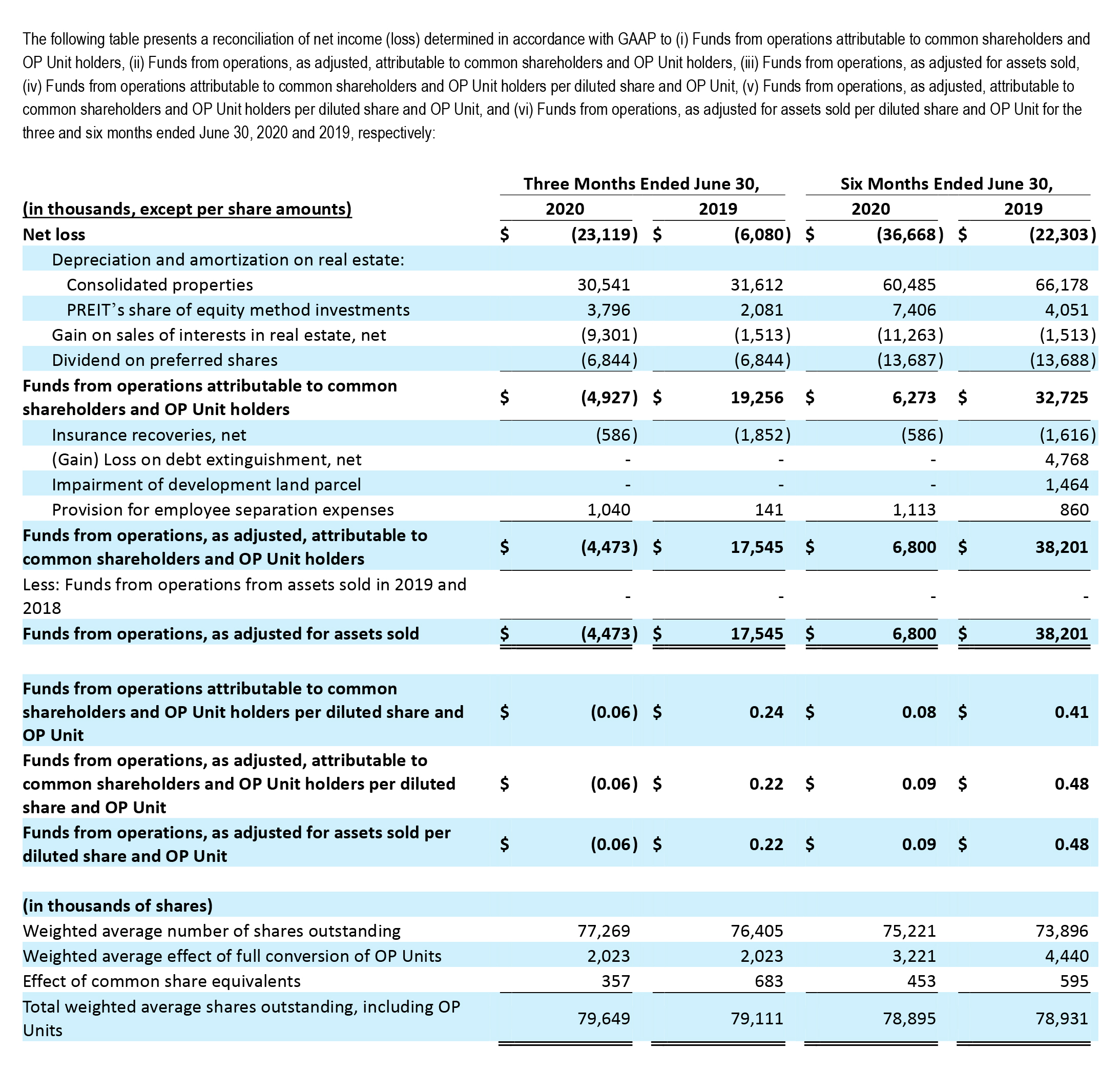

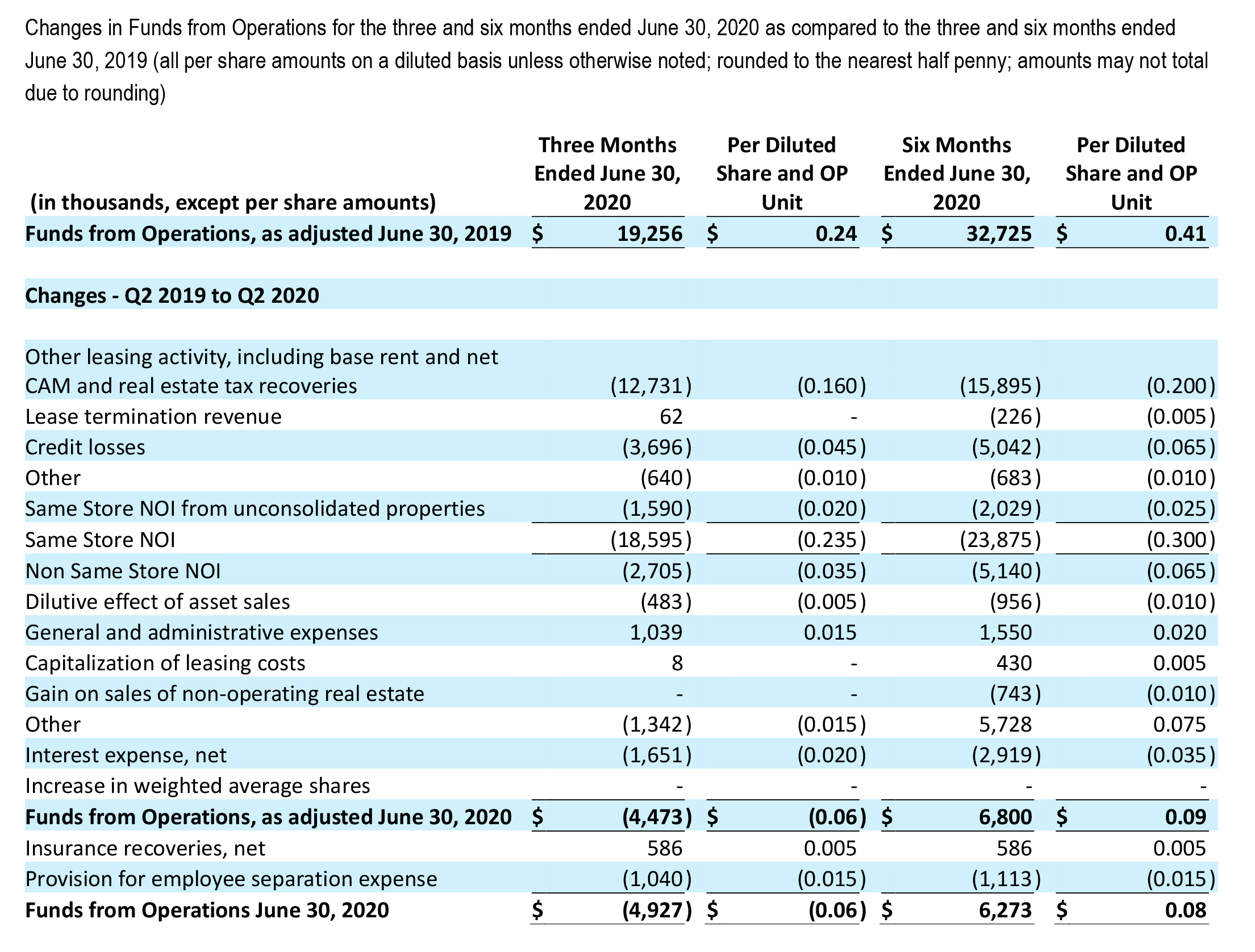

FFO for the three months ended June 30, 2020 was $(0.06) per diluted share and OP Unit compared to $0.24 per diluted share and OP Unit for the three months ended June 30, 2019. Adjustments to FFO in the second quarter of 2020 were less than $0.01 per share of provision for employee separation expenses. Adjustments to FFO in the 2019 quarter included $0.02 per share of Insurance recoveries.

General and administrative expenses decreased by $1.0 million compared to the second quarter of 2019 due to lower payroll and incentive compensation expenses.

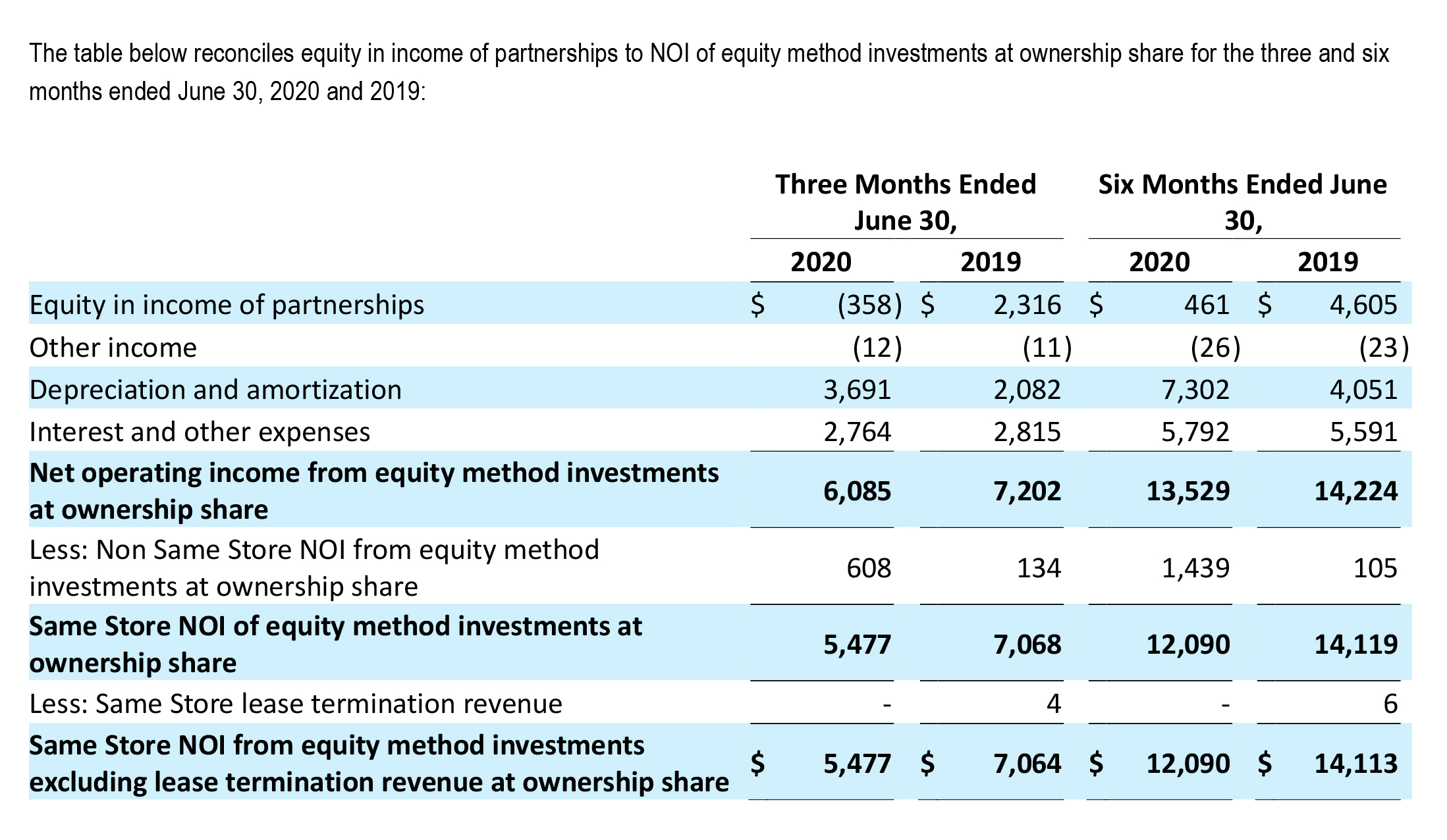

All NOI and FFO amounts referenced as primary factors affecting financial results above include our share of unconsolidated properties’ revenues and expenses. Additional information regarding changes in operating results for the three months ended June 30, 2020 and 2019 is included on page 16.

Asset Dispositions

During June, the Company completed our single tenant outparcel sale initiative, closing on the remaining $14.4 million in sales, bringing the total outparcel sale effort gross proceeds to $27.8 million.

Sale/Leaseback: In February 2020, the Company entered into an agreement of sale for the sale and leaseback of five properties for $153.6 million. Structured as a 99-year lease with an option to repurchase, the agreement provides for release of parcels related to multifamily development and is subject to ongoing lease payments at 7% ($10.75 million) with annual 1.25% escalations. Closing on the transaction is subject to customary closing conditions, including due diligence provisions.

Multifamily Land Parcels: The Company has executed agreements of sale for land parcels for anticipated multifamily development in the amount of $107.3 million. The agreements are with three different buyers across five properties for 2,650 units as part of Phase I of the Company’s previously announced multifamily land sale plan. Closing on the transactions is subject to customary due diligence provisions and securing entitlements. One buyer for two other land parcels had terminated its agreement and PREIT has now executed letters of intent with another buyer.

Hotel Parcels: The Company has executed two agreements of sale to convey land parcels for anticipated hotel development in the amount of $3.75 million. The agreements are with two separate buyers for approximately 250 rooms. Closings on the transactions are subject to customary due diligence provisions and securing entitlements.

Retail Operations

Due to COVID-related mall closures impacting the majority of the quarter, the Company is not reporting tenant sales at this time.

2020 Outlook

On March 31, 2020, the Company withdrew its financial outlook for 2020 provided in its February 25, 2020 earnings press release. The Company is not providing updated guidance at this time.

Conference Call Information

Management has scheduled a conference call for 9:00 a.m. Eastern Time on Tuesday

August 11, 2020, to review the Company’s results and future outlook. To listen to the call, please dial 1-844-885-9139 (domestic toll free), or 1-647-689-4441 (international), and request to join the PREIT call, Conference ID 4292929, at least fifteen minutes before the scheduled start time as callers could experience delays. Investors can also access the call in a “listen only” mode via the internet at the Company’s website, preit.com. Please allow extra time prior to the call to visit the site and download the necessary software to listen to the Internet broadcast. Financial and statistical information expected to be discussed on the call will also be available on the Company’s website.

For interested individuals unable to join the conference call, the online archive of the webcast will also be available for one year following the call.

Rounding

Certain summarized information in the tables above may not total due to rounding.

Definitions

Funds From Operations (FFO)

The National Association of Real Estate Investment Trusts (“NAREIT”) defines FFO, which is a non-GAAP measure commonly used by REITs, as net income (computed in accordance with GAAP) excluding (i) depreciation and amortization related to real estate, (ii) gains and losses from the sale of certain real estate assets, (iii) gains and losses from change in control, and (iv) impairment write-downs of certain real estate assets and investments in entities when the impairment is directly attributable to decreases in the value of depreciable real estate held by the entity. We compute FFO in accordance with standards established by NAREIT, which may not be comparable to FFO reported by other REITs that do not define the term in accordance with the current NAREIT definition, or that interpret the current NAREIT definition differently than we do.

FFO is a commonly used measure of operating performance and profitability among REITs. We use FFO and FFO per diluted share and unit of limited partnership interest in our operating partnership (“OP Unit”) and, when applicable, related measures such as Funds From Operations, as adjusted, in measuring our performance against our peers and as one of the performance measures for determining incentive compensation amounts earned under certain of our performance-based executive compensation programs.

FFO does not include gains and losses on sales of operating real estate assets or impairment write downs of depreciable real estate, which are included in the determination of net income in accordance with GAAP. Accordingly, FFO is not a comprehensive measure of our operating cash flows. In addition, since FFO does not include depreciation on real estate assets, FFO may not be a useful performance measure when comparing our operating performance to that of other non-real estate commercial enterprises. We compensate for these limitations by using FFO in conjunction with other GAAP financial performance measures, such as net income and net cash provided by operating activities, and other non-GAAP financial performance measures, such as NOI. FFO does not represent cash generated from operating activities in accordance with GAAP and should not be considered to be an alternative to net income (determined in accordance with GAAP) as an indication of our financial performance or to be an alternative to cash flow from operating activities (determined in accordance with GAAP) as a measure of our liquidity, nor is it indicative of funds available for our cash needs, including our ability to make cash distributions. We believe that net income is the most directly comparable GAAP measurement to FFO.

When applicable, we also present Funds From Operations, as adjusted, and Funds From Operations per diluted share and OP Unit, as adjusted, which are non-GAAP measures, to show the effect of such items as gain or loss on debt extinguishment (including accelerated amortization of financing costs), impairment of assets, provision for employee separation expense, and insurance recoveries or losses, net, which can have a significant effect on our results of operations, but are not, in our opinion, indicative of our operating performance. We also present FFO on a further adjusted basis to isolate the impact on FFO caused by property dispositions.

We believe that FFO is helpful to management and investors as a measure of operating performance because it excludes various items included in net income that do not relate to or are not indicative of operating performance, such as gains on sales of operating real estate and depreciation and amortization of real estate, among others. We believe that Funds From Operations, as adjusted, is helpful to management and investors as a measure of operating performance because it adjusts FFO to exclude items that management does not believe are indicative of our operating performance, such as provision for employee separation expense, loss on debt extinguishment (including accelerated amortization of financing costs) and insurance losses and recoveries.

Net Operating Income (“NOI”)

NOI (a non-GAAP measure) is derived from real estate revenue (determined in accordance with GAAP, including lease termination revenue), minus property operating expenses (determined in accordance with GAAP), plus our pro rata share of revenue and property operating expenses of our unconsolidated partnership investments. NOI does not represent cash generated from operating activities in accordance with GAAP and should not be considered to be an alternative to net income (determined in accordance with GAAP) as an indication of our financial performance or to be an alternative to cash flow from operating activities (determined in accordance with GAAP) as a measure of our liquidity. It is not indicative of funds available for our cash needs, including our ability to make cash distributions. We believe that NOI is helpful to management and investors as a measure of operating performance because it is an indicator of the return on property investment, and provides a method of comparing property performance over time. We believe that net income is the most directly comparable GAAP measurement to NOI.

NOI excludes other income, general and administrative expenses, provision for employee separation expenses, interest expense, depreciation and amortization, impairment of assets, equity in income of partnerships, gains/losses and adjustments to gains/losses on sales of interest in non operating real estate, gains/losses and adjustments to gains/losses on sales of interest in real estate by equity method investee, gains/losses on sales of interests in real estate, net, project costs, gain or loss on debt extinguishment, insurance losses or recoveries, net and other expenses.

Same Store NOI is calculated using retail properties owned for the full periods presented and excludes properties acquired, disposed, under redevelopment or designated as non-core during the periods presented. In 2019, Wyoming Valley, Exton Square and Valley View Malls were designated as non-core and are excluded from Same Store NOI. In 2020, Exton Square and Valley View Malls are designated as non-core and are excluded from Same Store NOI. Non Same Store NOI is calculated using the retail properties excluded from the calculation of Same Store NOI.

Financial Information of our Unconsolidated Properties

The non-GAAP financial measures of FFO and NOI presented in this press release incorporate financial information attributable to our share of unconsolidated properties. This proportionate financial information is also non-GAAP financial information, but we believe that it is helpful information because it reflects the proportionate contribution from our unconsolidated properties that are owned through investments accounted for under GAAP using the equity method of accounting. Under such method, earnings from these unconsolidated partnerships are recorded in our statements of operations prepared in accordance with GAAP under the caption entitled “Equity in income of partnerships.”

To derive the proportionate financial information from our unconsolidated properties, we multiplied the percentage of our economic interest in each partnership on a property-by-property basis by each line item. Under the partnership agreements relating to our current unconsolidated partnerships with third parties, we own a 25% to 50% economic interest in such partnerships, and there are generally no provisions in such partnership agreements relating to special non-proportionate allocations of income or loss, and there are no preferred or priority returns of capital or other similar provisions. While this method approximates our indirect economic interest in our pro rata share of the revenue and expenses of our unconsolidated partnerships, we do not have a direct legal claim to the assets, liabilities, revenues or expenses of the unconsolidated partnerships beyond our rights as an equity owner in the event of any liquidation of such entity. Our percentage ownership is not necessarily indicative of the legal and economic implications of our ownership interest. Accordingly, NOI and FFO results based on our share of the results of unconsolidated partnerships do not represent cash generated from our investments in these partnerships.

Core Properties

Core Properties include all operating retail properties except for Exton Square Mall, Valley View Mall and Fashion District Philadelphia. Core Malls excludes these properties, power centers and Gloucester Premium Outlets.

Forward Looking Statements

This press release contains certain forward-looking statements that can be identified by the use of words such as “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “project” or similar expressions. Forward-looking statements relate to expectations, beliefs, projections, future plans, strategies, anticipated events, trends and other matters, including our expectations regarding the impact of COVID-19 on our business, that are not historical facts. These forward-looking statements reflect our current views about future events, achievements, results, cost reductions, dividend payments and the impact of COVID-19 and are subject to risks, uncertainties and changes in circumstances that might cause future events, achievements or results to differ materially from those expressed or implied by the forward-looking statements. In particular, our business might be materially and adversely affected by the following:

- the COVID-19 global pandemic and the public health and governmental actions in response, which have and may continue to exacerbate many of the risks listed below;

- our ability to implement plans and initiatives to adequately address the “going concern” considerations described in Note 1 to our consolidated financial statements in our Form 10-K for the year ended December 31, 2019;

- changes in the retail and real estate industries, including consolidation and store closings, particularly among anchor tenants;

- current economic conditions, including current high rates of unemployment and its effects on consumer confidence and spending, and the corresponding effects on tenant business performance, prospects, solvency and leasing decisions;

- our inability to collect rent due to the bankruptcy or insolvency of tenants or otherwise;

- our ability to maintain and increase property occupancy, sales and rental rates;

- increases in operating costs that cannot be passed on to tenants;

- the effects of online shopping and other uses of technology on our retail tenants;

- risks related to our development and redevelopment activities, including delays, cost overruns and our inability to reach projected occupancy or rental rates;

- acts of violence at malls, including our properties, or at other similar spaces, and the potential effect on traffic and sales;

- our ability to sell properties that we seek to dispose of or our ability to obtain prices we seek;

- potential losses on impairment of certain long-lived assets, such as real estate, including losses that we might be required to record in connection with any disposition of assets;

- our substantial debt and the liquidation preference of our preferred shares and our high leverage ratio and our ability to remain in compliance with our financial covenants and obtain additional debt covenant relief under our debt facilities;

- our ability to refinance our existing indebtedness when it matures, on favorable terms or at all;

- our ability to satisfy our indebtedness if such indebtedness were to be accelerated due to breach of covenants or payment default, as well as our ability to satisfy any other debt that was accelerated as a consequence;

- our ability to raise capital, including through sales of properties or interests in properties and through the issuance of equity or equity-related securities if market conditions are favorable;

- our ability to continue to pay dividends at current levels or at all; and

- potential dilution from any capital raising transactions or other equity issuances.

Additional factors that might cause future events, achievements or results to differ materially from those expressed or implied by our forward-looking statements include those discussed herein and in the sections entitled “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2019 and in our Quarterly Report on Form 10-Q for the quarterly period ended March 31, 2020 and any subsequent reports we may file with the SEC. We do not intend to update or revise any forward-looking statements to reflect new information, future events or otherwise.

** Quarterly supplemental financial and operating information will be available on www.preit.com **

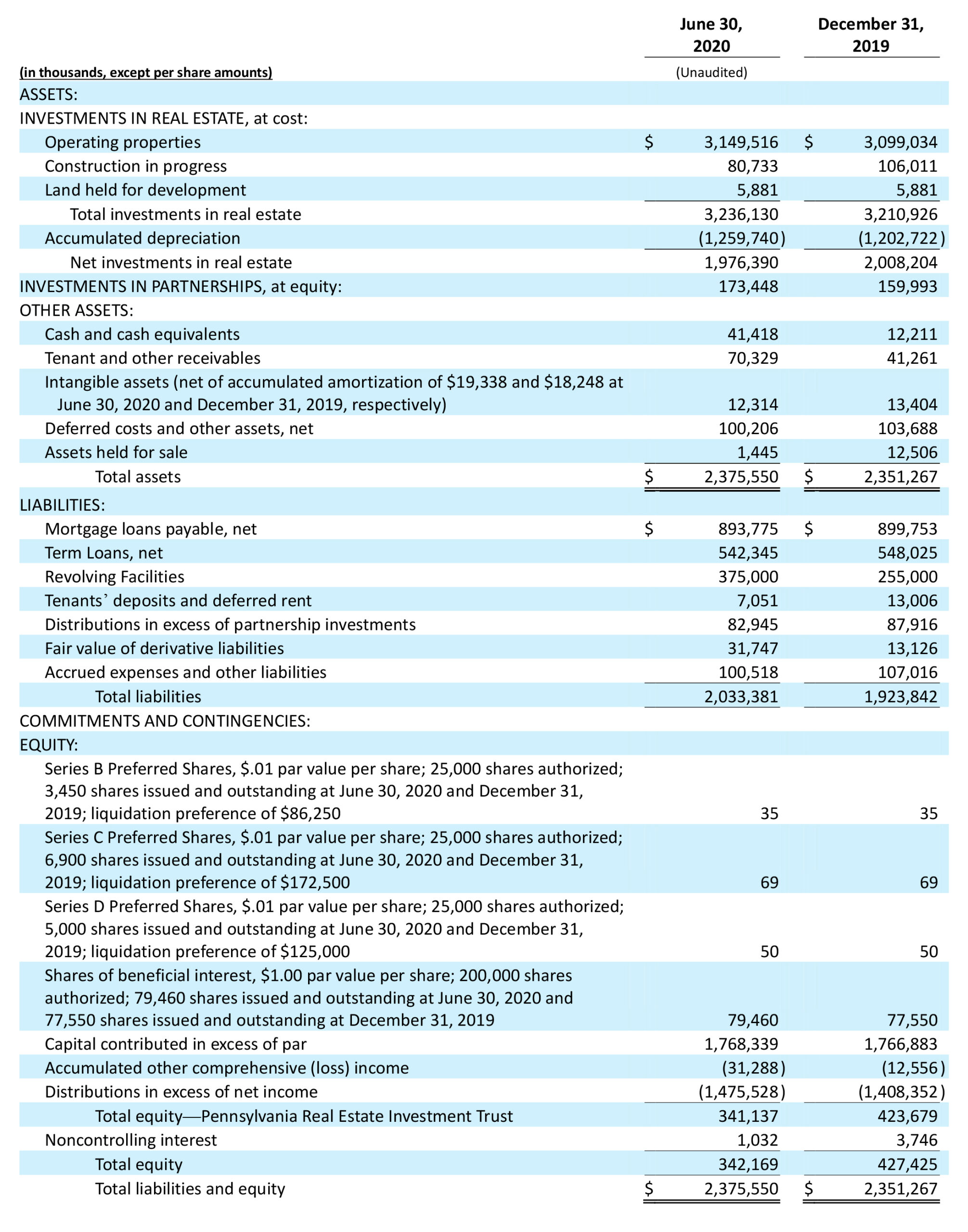

Selected Financial Data